R&D Tax Credits are a Big Deal for any business, including cannabis.

What is the R&D Tax Credit?

The R&D Tax Credit (26 U.S. Code §41) is a federal benefit that provides companies dollar-for-dollar cash savings for performing activities related to the development, design, or improvement of products, processes, formulas, or software

The R&D tax credit is a very powerful credit available to pretty much any organization, regardless of business type. They are available by federal law forever and are also available in a large number of state tax laws.

Many cannabis companies, both CBD and THC-based have barely even existed for more than five years. This means you're probably spending a good deal of money on developing new products and processes. For federal purposes cannabis businesses subject to 280E, the credits will likely only apply against payroll taxes but this can still produce a significant benefit to businesses that take the time to understand the tax code and implement projects that qualify. This is where Greenbooks can help. Our understanding of R&D tax credits, combined with our experience in 280E/cannabis put us in the position to help our customers take full advantage of these lucrative tax benefits.

So why aren’t cannabis operators taking advantage?

R&D tax credits for cannabis businesses can be substantial. As an example, you can earn up to 10% of wages paid to employees who work on R&D projects.

So why are so few cannabis businesses claiming them?

The answer is simple: very few people are even aware that the federal government and many states offer tax incentives for businesses that create new products, processes, and innovate. In the cannabis industry, this requirement can apply to many manufacturers, cultivators, and labs in particular.

There is also a common misconception that 280e would automatically disallow any tax credits but 280e applies only to income tax; the switch to payroll tax negates this. This is also why cannabis companies are eligible for ERC.

Do I qualify for R&D Tax Credits?

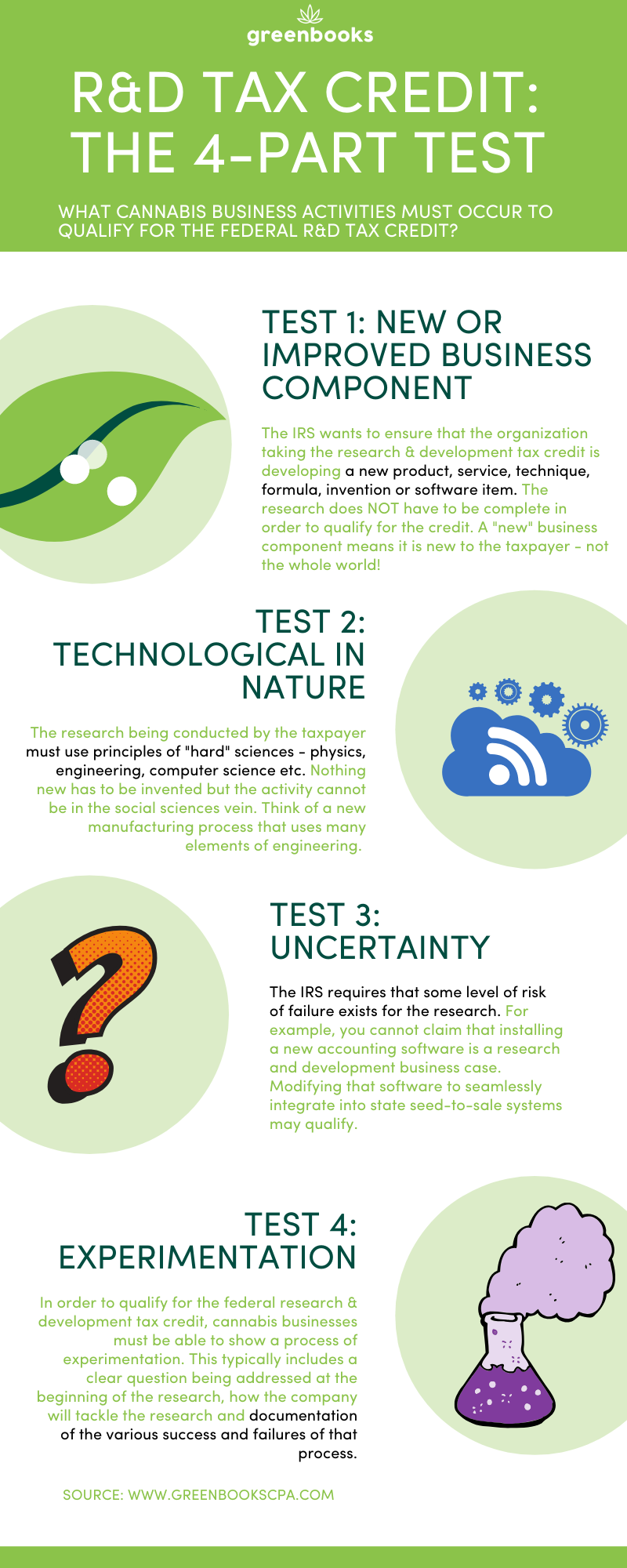

Any business can qualify for R&D tax credits by meeting the four-part test.

Test #1: New or Improved Business Component: Developing a new product, service, technique, formula, invention or software item.

Test #2: Technological In Nature: The research being conducted by the taxpayer must use principles of “hard” sciences, physics, engineering, computer science, etc.

Test #3: Uncertainty: Some level of realized or potential failure must exist.

Test #4: Experimentation: The taxpayer must show a process of experimentation.

While these qualifications may sound complicated and scientific, by understanding them in more detail and applying them to your business you will likely find them to be very advantageous and quite easy to qualify for by simply applying this four-part test:

Now you may still be thinking that this is complicated and that it may be too difficult to apply these principles to a cannabis business. Here are a few examples where very standard activities may qualify by business type.

Cannabis Manufacturers

* New manufacturing processes to produce a better, higher-quality, more efficient yield (new distillate, extraction process)

* A packaging process that results in less waste product.

* A new container design that provides more efficiency or better quality.

* New process for infusing THC into food, drinks, and any consumables.

Cannabis Cultivators

* Development of a new or improved strain.

* Implement & test new processes such as lighting application, soil, fertilizer, nutrients, watering, different UV products, etc.

Cannabis Labs

* New testing processes (testing CBG %, have never tested and need new process)

* Any custom work may qualify, non-standard processes

* Software and testing process improvements

If the business activity fits all four requirements, it is likely eligible for the federal R&D tax credit. If your cannabis company is relatively new, chances are that quite a bit of your activity falls under this umbrella. With no hard cap, the R&D tax credit is indeed a big blessing for the industry.

Determining Qualified Research Expenses

Now we will discuss the types of expenses that can be claimed in the R&D tax credit program. As a general rule, and for most businesses, the following types of expenses can be considered.

Wages

Supplies

Contract Research

Note: THC businesses can include supplies and contract research in their calculation as well, however they can only apply the credit to payroll tax (Federal Income Tax not eligible)

Wages: Typically your heaviest hitter, the W2 taxable salary paid to each employee can be calculated as part of the R&D tax credit based on the percentage of the time the employee worked on an R&D project. To give you an idea of how this applies, suppose you had a regular cannabis cultivator who made $80,000 a year in base salary plus equity. If half of this employee's time was dedicated entirely to researching and applying new growing methodologies to increase yield, potentially $40,000 could be a Qualified Research Expense for the company. As a rule of thumb, you could potentially earn up to 10% of those qualifying wages. There are three tiers of employees whose wages can qualify:

(1) the direct researcher doing the actual research and development

(2) the direct support helping this individual on their R&D quest, typically with prototype testing and quality assurance

(3) the direct supervision such as the direct researcher's manager, at whatever allocation of time was spent reviewing the work. Executive wages ARE allowed here so for folks running a lean shop, maybe the CEO is overseeing the research which is just fine.

Supplies: Supplies include raw materials used for prototype or testing the new product/process. For manufacturers, some examples include bulk flower, trim, and other elements purchased for the experimentation to create the product. A cannabis cultivator could include seeds, soils, and grow supplies that the company purchased specifically to test the new growing methodology. There are limitations. For example, depreciable property is not allowed to be rolled into the credit. Additionally, you cannot include general & administration expenses into this category (i.e. electrical bills)

Contract Research: Contract research expenses are when the taxpayer hires a third party to conduct research on its behalf (i.e. a contractor, contract worker, or a third-party business). Using the cultivator example, let's say the employee is on the precipice of a new growing methodology but can't quite finish their experiment. If the research was contracted to be completed by a third party, those expenses may be able to qualify here. Generally speaking, the rule for contract research is that whoever is claiming the tax credit must retain ownership rights of the research. For the cannabis industry specifically, contract research expenses include certification testing. So for our CBD friends, if you have your product tested by a third party to ensure quality, those costs will qualify. Similarly, for THC companies, whatever state-mandated testing your product goes through could potentially qualify as R&D tax credit expenses. Eventually, we will have to all become FDA-approved, which means those costs down the road will fall in here.

The big takeaway here is ultimately wages will probably be the key driver for your actual qualified expenses, followed by contract research and then supplies. Don't forget - costs relating to certifications may be qualified expenses so be sure to keep track of those costs.

How to Utilize the Credit

I bet you are starting to understand why this tax credit can go such a long way in the cannabis industry. With all of the new products, and innovation in cultivating and manufacturing we've seen in such a short span, we should easily be claiming billions of dollars in this credit. Another awesome thing about the credit is it can be used in a variety of ways. The federal research & development tax credit can be used to:

Offset Federal Income Tax

Offset a portion of Payroll Tax (for qualified cannabis startup businesses)

Federal Income Tax

The first option is the classic option for pretty much any tax credit. Some portion of your R&D tax credit can offset your federal income tax liability. Going back to the original purpose of the credit, the government wants to incentivize innovative behavior and will help you pay some bills along the way. Keep in mind you must either pick payroll application or income tax application for any given year.

But what if you're operating at a loss or don't owe any money?

Payroll Tax (qualified cannabis startup businesses)

Beginning in 2016 qualified startup businesses may now use the R&D tax credit to offset some portion of their payroll tax. This is an outstanding development for us in the cannabis industry as it opens the playing field for marijuana companies to begin claiming this credit. For this definition, a startup business is a company with less than $5 million in gross receipts. This is also a good news story for organizations that are still producing a small or no income tax liability. Payroll taxes are mandatory regardless of income and thus we can take a portion of your R&D tax credit and apply it in the current period regardless of how much money you're making.

Best Practices for Claiming the R&D Tax Credit

The cannabis industry still has an issue with proper documentation. We see it all the time as accountants; handshake deals, poor record keeping, and unclear work papers. The IRS tends to be protective of tax credits and the R&D credit is no different. They expect a level of documentation the cannabis industry tends to be lacking. To confidently claim the credit and substantiate your claim in the event of an audit, the cannabis company should adhere to certain standards of documentation including:

Financial expenses

Project expenses such as supplies and new resources needed

Organizational expenses based on qualifying employees percentage of time spent on the project

As we discussed above, only certain types of costs may fall under the category of Qualified Research Expenses for the R&D tax credit. Therefore it is important to keep very detailed documentation in terms of how you arrived at the numbers presented to the IRS. Most often you'll find yourself preparing a spreadsheet as you'll have to allocate employee's time to R&D-qualified and non-qualified business activities throughout the year. Similarly, for any expenses being taken for supplies, it should be clear how you came to a monetary figure. Ideally, those costs came from a single purchase order. And of course, the same should apply to any contract research and certification testing. In a perfect world, you would have all of this maintained and bundled ready to hand over to an IRS auditor at any time explaining both the figures and assumptions that went into them.

For project documentation when claiming the R & D tax credit, the IRS wants to validate that the project was pre-considered by the company and had an end goal in mind. What they DON'T want is for cannabis companies to staple together a bunch of random costs and call it a research and development project. To best protect yourself, you would ideally keep some project documentation for each type of R&D type activity your company is taking on. In that project documentation, you want to discuss the project narrative. Some common items would be why did we start this research? What was the end goal? In what ways does the research benefit the company? On top of a project narrative, any additional supporting documentation will help such as time sheets, e-mail communications internally and externally discussing the intended scope, etc.

Finally, you may want to consider additional documentation regarding organizational responsibilities. A good place to start is clear job descriptions. If you are hiring a new cannabis cultivator for example, it would be prudent to include in the job description any possible research and development type activities that may be expected from that role. For larger companies, you may want to specify which employees are considered part of the R&D department, and what their responsibilities and expectations are.

In Summary

R&D tax credits can make a big impact and too few businesses in the cannabis industry are taking advantage. Just think of all the innovation that is taking place in your business. Why would you want to leave that money on the table? There are qualifications and requirements and that is where we come in.

Don’t miss this opportunity!!! Contact Greenbooks CPA today and schedule a free consultation with one of our CPAs to determine if you are missing out on the opportunity to increase your profits.